Part I: Asset-Backed Line of Credit Products Will Go Mainstream This Decade

Part I: Asset-Backed Line of Credit Products Will Go Mainstream This Decade

Rise of Asset-Backed Line of Credit Products

This decade, asset-backed line of credit products will go mainstream. With these products, you can access liquidity without selling your assets. This means you continue to maintain ownership of your assets and enjoy the upside. Because you don't sell you also avoid paying capital gains tax.

Currently, only the ultra-wealthy commonly use these products. Lately, the press has covered how ultra-wealthy use these products as part of their buy, borrow, die strategy. But there will be two developments across the next decade which will make these products go mainstream. First, the opportunity cost of not using this strategy will increase as financial asset inflation picks up and capital gains tax rates get hiked. Second, more assets will move on-chain and users gain self-custody of assets. This will expand product options and lead to more frictionless experiences.

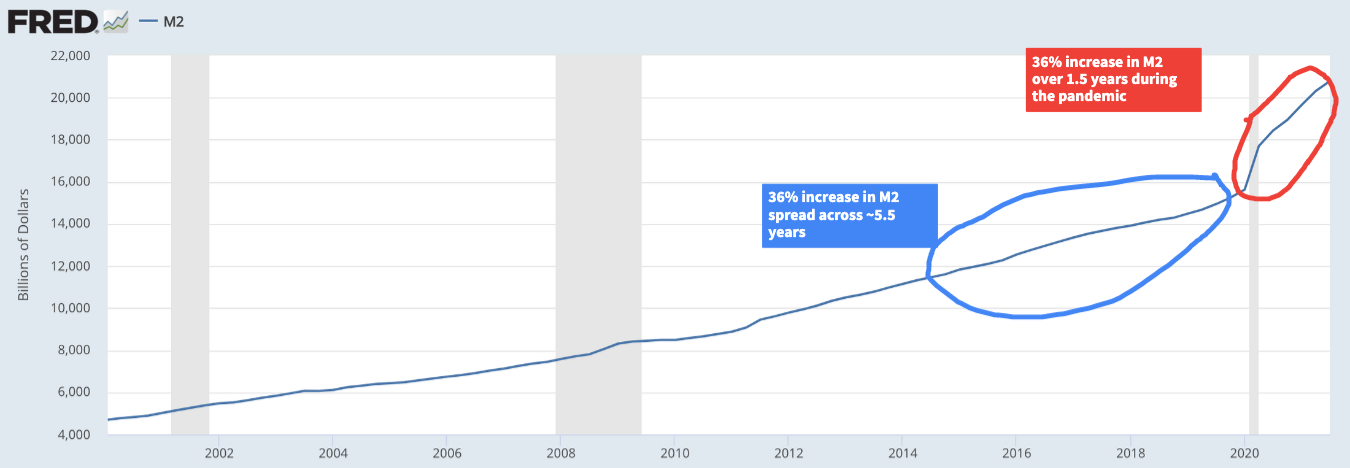

Money Printer Goes Brr… Asset Prices Begin to Moon

Following the 2020 pandemic, the Federal Reserve injected an unprecedented level of monetary stimulus. M2 (i.e., Near Money) supply- which measures savings deposits, money market securities, and mutual funds- increased 36 percent within the last 1.5 years. It took 5.5 years for the M2 to increase by the amount before that. This money has to flow somewhere. So it isn't surprising, that we see inflation in both consumer goods and financial assets.

Yet, I am skeptical that inflation in consumer goods (e.g., food, automobiles) will persist. Technology, globalization, combined with an aging population act as powerful deflationary forces. Teething supply chain issues like the chip shortage exist. But there is enough economic incentive to resolve them. These supply chain will likely dissipate soon.

What will continue unabated is the financial asset inflation. We are seeing a boom across every asset class. Real estate, equities, crypto are all up double or triple digits over the past year. The Fed is severely constrained in its ability to raise interest rates. The economy has become addicted to cheap debt. Even if interest rates creep up marginally, it could threaten a fragile economy. For one, the federal government will struggle to meet its debt obligations. With federal debt hovering just above the GDP, meeting debt obligations will become much tougher to service. Additionally, zombie companies1, like Carnival Cruise and Macy's, estimated to make up 20% of all large public companies, will layoff many setting off an unemployment crisis. The upshot: The Fed will likely maintain accommodative monetary policy for the foreseeable future. This will support further asset price increases. If you hold large amounts of cash, you are losing. You want to stay as invested as possible to maximize your returns.

Demand for Asset-Backed Line of Credit Products Will Increase

Even though you want to stay fully invested, you will have occasional liquidity needs to meet. You need fiat money to pay for your children's tuition and home mortgage. But selling your assets wouldn’t be financially savvy because you then miss out on gains from asset appreciation.

Additionally, when you sell your assets, you become liable to pay capital gains tax. The actual tax rate can range between between 15% to 40% depending on your income and how long you held the asset. Across the next decade, the government will likely hike the capital gains tax to generate more revenue and address rising wealth inequality concerns. This will make selling assets to meet cash needs even less appealing.

DeFi will Enable Users to Access Asset-Backed Loans Frictionlessly

There are asset-backed line of credit products that mainstream users can access now. Examples include Home Equity Line of Credit (HELOC) at many major banks or Securities-Backed Line of Credit (SBLOC) at specific brokerages such as Charles Schwab. But options are limited. These products can also be cumbersome to use.

In the future, as DeFi expands users will gain easier access to these asset-backed line of credit products. Why? Now, users entrust institutions to hold custody of their assets. Loan providers need to access and sell your collateral in case you don't pay back the loan. This means of one of two things. Either, the current institution with custody of your asset provides this product (e.g, Charles Schwab, Coinbase). Or, you have to transfer your assets to the loan provider. This means now you have to tradeoff between convenience and having more options. This will change as DeFi expands and more assets move on-chain. The blockchain enables you to have self-custody of your assets and easy transfers. More DeFi asset-backed lending protocols will emerge to take advantage of this. Also, DeFi protocols are nimbler than existing financial institutions. The reduced overhead will translate to lower costs and better experiences.

Addressing Margin Call Risk in Asset-Backed Loans is Necessary for Mainstream Adoption

The increased desire to satisfy liquidity needs with asset-backed loan combined with the greater convenience of getting one will make more people interested to take this route. But, there's one major risk that needs to be mitigated or eliminated if these products are to go mainstream: margin call.

Every loan provider sets their own expected loan-to-value (LTV) ratio. You calculate the LTV ratio by dividing the loan's value over the collateral's value. But the collateral's price can drop after the loan issued. Suppose, you took a loan of $50k on a $100k worth of Bitcoin. This means the LTV is 50%. But suppose, Bitcoin's value drops 30% - an eminent possibility. Now, the LTV ratio drops to 71%, below the required 75%. At this point, you have to pay back some of the loan back or post more collateral to maintain the required LTV ratio. Otherwise, the loan provider will liquidate some of assets.

Unless loan providers address the margin call risk, growth in these financial products will be muted. There are a few reasons for this. First, unlike the ultra-wealthy, mainstream users may not have much more financial surplus. This means they will be more limited to pledge additional collateral. Second, the constant fear that there could be a crash and one's positions will get liquidated is a stressful experience. And if a margin call does happen and one's collateral gets liquidated, it leaves a very sour taste.

In the next part, I will discuss two different ways asset-backed line of credit products can be designed to address the margin call risk highlighted above.

Disclaimer: Nothing presented here is financial advice. Do your own research.

I am very actively exploring crypto-backed line of credit products in DeFi space. If you are interested or work in this sort of stuff, DM me.

Zombie companies are companies which don't generate enough income to meet their debt obligations

Very thoughtful and engaging work on the future trajectory of finance